Close cooperation among all stakeholders is necessary in order for the health insurance business to succeed, says Mr Mahomed Akoob of Hannover ReTakaful.

The health industry globally is slated to grow at a pace faster than ever before. The next few years will see increased demand for health coverage from affluent customers, corporate organisations and mandatory health insurance regimes.

Insurers certainly stand to benefit from such unprecedented growth for this line of business. The inherent risk characteristics are also supposed to change, influenced by demography, lifestyle and morbidity patterns. And naturally, the proliferation of risk is bound to require more capacity and expertise from the reinsurance industry.

From the reinsurer’s viewpoint, the health business is seen as a frequency business with a relatively predictable stream of claims. This means that the direct insurer experiences attritional losses with few severity spikes. In most instances, reinsurance is bought either for solvency relief or where the reinsurer is entrusted to quantify the risk.

The appetite for health risk

The quantification of health risk is a particularly interesting subject. In this regard, claims data with relevant qualitative attributes is an indispensable tool with respect to arriving at an equitable premium for the risk in question. Many times, direct insurers have fragmented systems and their data sets do not seem to meet qualitative attributes, raising questions about data credibility.

Keeping in view the business opportunity, it is unsurprising to see several small to medium reinsurers building their appetite for health risk. These new entrants employ aggressive pricing offers to penetrate the market, which allow market entry but in the medium to long term, run the risk of heavy losses. These risk-assuming companies then fail to support the market in the long run and depart from the market with poor bottom-line results.

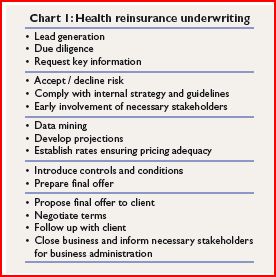

Steps in reinsurance underwriting

Reinsurance underwriting of the health business, as such, is an intricate multi-step process. It begins with evaluating the suitability of the proposal, assessing the prospect and its business plan, analysing historical performance, identifying claims control and rate-making, and culminates with proposal generation and submission.

Chart 1 briefly describes the entire process.

The key information in this instance includes the company and management profile, economic/ political background, financial profile, business plan, estimated premium income, inception date and historical claims data.

Key challenges

Today, the quality of available data is an extremely big challenge facing the reinsurance industry. The top reinsurers, however, ensure by nature and spread of their business, market-wide exposures and necessary expertise to translate the data sets they receive into meaningful results. Of course, for stable portfolios with decent critical mass and credible data, the analysis leads to fairly accurate estimates of the expected cost of future claims.

Reporting lags and under-reserving, however are serious concerns for the reinsurance industry. The delay in reporting could be either due to an untimely receipt of bills by the direct insurer, or due to inefficient claims processing by the in-house team or third-party administrators (TPAs). In any case, the result is aberration of claims data which fails to reflect the true claims development. Under-reserving also leads to a similar situation wherein incurred but not reported (IBNR) claims are neither properly estimated nor plugged into the ultimate claims development and pose a significant risk for proportional long-tail business.

As the awareness amongst the masses grows, so does the utilisation and the burning cost. Under these circumstances, neither the insurer nor the reinsurer would like to be outpaced by the cost of claims that make the entire business proposition unviable. Hence, the premiums in general also require periodic adjustment and in accordance with latest utilisation trends. To address the issue, reinsurers require monthly portfolio performance reports. Then, on the basis of quarterly trends, a rating review is carried out to ensure the portfolio remains sustainable.

Unlike the past, revenues from investment income add little to the results. Hence, direct insurers and reinsurers need to stress on developing holistic risk management and underwriting guidelines for positive bottom-line results. On the direct side, this includes human capital management, designing market-specific guidelines and consulting with the reinsurer for risks exceeding the delegated authority. It is also important that the reinsurance structure is set up with appropriate risk transfer, alignment of interest and focus on technical profitability.

Stakeholder cooperation

Involvement of all potential stakeholders early during the reinsurance setup process is crucial in successful business placement. As reinsurers work on a global scope, it is imperative they understand the local regulatory environment of their prospects and cedants. The regulators, brokers, cedants and TPAs are other stakeholders that need to work in coordination with each other to ensure that results meet expectations.

Regulators

An interested regulator creates a framework which is the recipe for a thriving health business. Hence, for reinsurers who transact business globally, it is extremely important they understand health-specific guidelines for business regulation and compliance that applies to operators transacting health business – TPAs as well as providers in various territories.

TPAs

TPAs engaged by direct insurers play a very important role in the entire business value chain. Their role is not limited to network management, tariff negotiation, volume discounts, claims processing and cross-border facilities. The volume of business TPAs handle allow them to negotiate preferential treatment rates with providers, which in return translates to a decreased claims cost for the direct insurer.

Direct insurers

Following market developments, retention ratios for direct insurers are also on the rise. Many players, especially the experienced ones with sizeable critical mass and profitable portfolios, prefer to retain most of the risk on proportional basis. A non-proportional solution with higher priorities is another option these players are comfortable with. From the reinsurer’s perspective, this approach is highly appreciated as it reflects the fact that the direct players have appropriate expertise and are extremely confident in their methods of doing business.

Also, reinsurers by the nature of their business are not directly involved in the day-to-day account management of various policies that are ceded to the treaty. In this regard, it is very essential that the direct insurers have appropriate capabilities to combat fraud and abuse, manage the network of providers and employ cost containment measures.

Fraud and abuse

The health business has a high cost of inefficiency due to unwarranted use, identity theft and administrative system inefficiency. Fraud and abuse is an area which requires management through a dedicated team of expert professionals. Ineffective and wasteful use of healthcare resources account for unnecessary burdens on consumers who are obliged to pay for these costs indirectly in the form of higher premiums.

On the provider side, there is lack of care coordination, avoidable care and billing for expensive services but providing less expensive services in the healthcare system. By combatting fraud, the overall outgo on medical treatment will decrease substantially. The leakages could be minimised by direct insurers through provider surveillance and its compliance with disease management protocols.

Other cost containment measures stem from provider tariff regulations that prohibit indiscriminate increases through appropriate regulatory bodies. The pay-for-performance model in this regard could incentivise payment of providers based on their performance levels. The direct operators also need to ensure that patients do not utilise providers beyond their target network and hence attract an unintended higher claims cost.

Risk concentration

As the health business is high in volume but has marginal profitability, many direct insurers fall into the trap of concentrating too much on the health risk in the pursuit of the top line. Frequently, direct insurers also assume that the health business is a door opener to penetrate other business lines of policyholders.

Reinsurers should be very wary of this approach as risk concentration amongst various business lines is as important as health business mix and segmentation across various products. Hence, it is also necessary to balance the profitable individual health segment with the fastest-growing group health segment.

Managing claims

It is also observed in most markets that the group health segment’s lapse rates and policyholder loyalty are intertwined with claims experience. So, when an unfavourable experience attracts an increase in renewal premiums, the policyholder looks for alternatives and switches the insurer.

In this regard, it is worth pondering if domestic insurers should join hands to establish centralised claims repositories and information bureaus. This ensures competition is based not on price cuts but operational efficiency. In return, the support which the insurers expect to receive from reinsurers is also based on fair absolute cost of underlying claims.

Focussing on wellness and preventive programmes by direct insurers can also ensure reductions in claims costs for a simple reason. The cost of treating chronic diseases is a huge burden, in most cases a life-long burden in the form of maintenance therapies. By innovating and deploying preventive care solutions through insurance, many conditions can be diagnosed at a very early stage where intervention and full recovery is entirely possible.

At the end of the day, what is important is whether the elements in the value chain are able to deliver the solution desired by the consumer at a viable and affordable price. For this to happen, all involved stakeholders need to closely cooperate with each other besides continuously streamlining their processes and improving their capabilities.

Mr Mahomed Akoob is the Managing Director of Hannover ReTakaful.