Low penetration across most African markets spell many opportunities for insurers, but success will depend on their ability to devise strategies to expand their foothold in a continent of 54 immensely diverse economies.

Numbers are pointing to solid economic and demographic dynamics in Africa. According to the UN, the region’s GDP is expected to accelerate from 3.5% last year to 4.6% in 2015 and 4.9% in 2016 due to private investment and consumption. Other key drivers such as increasing consumer confidence, an expanding middle class, improvements in the business environment and lower costs of doing business have also contributed to the continent’s economic growth.

An earlier report by the World Bank projected the region’s GDP growth to strengthen to 5.2% yearly in 2015-16 from 4.6% in 2014, despite weaker-than-expected global growth and stable or declining commodity prices. Significant public investments in infrastructure, increased agricultural production and expanding services in African retail, telecoms, transportation, and finance, will help to boost growth.

Today, Africa is the second fastest-growing economic region in the world after Asia. Moreover, it is the only region where the population is projected to keep increasing throughout the 21st century, said UNICEF. By 2050, Africa’s population will double from the current 1.2 billion to 2.4 billion, eventually reaching 4.2 billion by the end of the century.

Foreign interest

The growth dynamics are benefitting many sectors of the economy, including insurance, and attracting rising interest from investors around the world, particularly mature markets such as the US and Europe.

For example, in the last few months, two global insurers announced plans to enter South Africa. In April, credit insurance company Euler Hermes said it is launching services for the market, and strengthening its presence on the African continent.

This followed a similar announcement in February of Swiss Re Corporate Solutions’ first local representation on the continent. Operations, which are expected to begin during the second quarter of 2015 from an office in Johannesburg, will provide commercial insurance services to mid- and large-sized corporate clients, focussing on property, mining and engineering risks, as well as customised solutions for the agriculture and energy sectors.

In the same month, AXA paid US$61 million to buy a 7.15% share of Africa Re. It affirmed its commitment to the continent, “where we believe insurance has a crucial role to play in promoting economic development, due to its contribution to improving risk management, protection and prevention”, the French insurance giant said. It also has a presence in Cameroon, Gabon, Ivory Coast, Senegal, Algeria, Morocco and Nigeria.

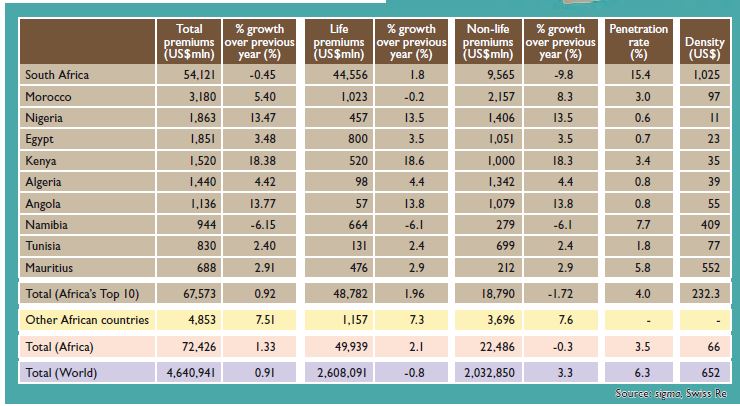

“In Africa, you find some of the fastest growing economies, dynamic demographics and a very low penetration rate for the insurance industry, ranking from 3% in Morocco and Ghana to 0.9% in Angola or 0.6% in Nigeria, compared to 7.6% in the Eurozone. There is no question that today, those are some of the most attractive markets worldwide for the insurance industry,” said Mr Jean-Laurent Granier, CEO of AXA’s Mediterranean and Latin America Region business unit and Chairman & CEO of AXA Global P&C, in charge of overseeing AXA Corporate Solutions’ global operations.

Low level of awareness

However, despite the developments, only 3.5% of the African market is insured, according to Swiss Re’s sigma report. Apart from South Africa (15.4%), Namibia (7.7%), and Mauritius (5.8%), all countries have very low penetration ratios. In addition, the insurance market is still relatively concentrated, with the top 10 of the 54 markets accounting for 93.3% of the $72.4 billion total premiums.

The low penetration has been attributed to factors including people’s lack of trust in financial service providers, and communities often making use of informal forms of insurance rather than using the services of formal insurers. There is also a lack of reliable information, making it challenging to assess people’s credit-worthiness.

The low level of awareness and education of insurance in the African markets is a major barrier to the sector’s progress, said Dr Femi Oyetunji, Group MD/ CEO of Continental Reinsurance. “Many people in Africa still do not consider insurance as a financial product. Economic factors are driving a new and emerging middle class with more disposable income, but the industry needs to drive efforts to raise awareness and understanding of insurance to generate and accelerate the potential growth.”

Mr Alex St James, Chief Operating and Underwriting Officer at One Re, added that a lack of human resource and requisite insurance expertise is exacerbated by the lack of investment into dedicated insurance training on the continent. “The failure to invest in local or even regional training centres for insurance proficiency is a very real risk to the development of the industry and the employment prospects of African insurance professionals in the global insurance industry,” he said.

“Training also has to consider and embrace the requirements for support services needed by the insurance industry, such as loss adjusting and surveying,” he said, adding that the lack of development of support services in the industry also means that these resources need to be imported from countries such as the UK.

Market fragmentation

Market fragmentation across a large number of countries and regulatory hurdles are further obstacles for the African insurance sector.

Currently, there is a plethora of local insurance companies in various African markets, with little collaboration among the operators. For example, Nigeria and Kenya currently have 50 insurance companies each, and Liberia – with a population of only 3.5 million – has about 20 insurance companies.

Local companies therefore need to consolidate to develop and achieve the business potential in Africa, Dr Oyetunji urged. “The competition in the African markets is steep, and premium rates are generally low because of the proliferation of insurance companies. The markets can do better and develop quicker if companies consolidate and collaborate,” he said.

“Without urgent attention given to consolidation and collaboration, African insurance markets are at the risk of being consumed by global players hungry to tap into Africa’s fast-growing economic emergence,” he warned.

The over-abundance of insurance companies in each market creates unnecessary competition which, rather than producing more affordable premiums, results in instability with regular swings in the pricing, said Mr St James. “Each new market entrant is forced to loss lead to gain sufficient market share to cover costs. There are just too many insurers chasing too few risks, with each successive renewal cycle seeing a movement of risk from one company to another at an ever-diminishing level of premium.”

Lack of consistent regulations

With the increase in the number of players and activities in the African insurance business, regulators have been stepping up their efforts to reform and establish effective supervision. However, said Mr St James, “regulators tend to be inadequately staffed or empowered to either enact market reform or to enforce market regulations. In most cases, the regulator acts as the ombudsman to the public”.

In addition, the “lack of consistent regulation in many markets lead to differences in accounting policies, reserving methodologies, risk management and business conduct, enabling poorly performing or technically insolvent (by international standards) companies to operate for many years without fear of regulatory intervention”, he added.

Knowing the market

As a continent of nations with populations ranging from less than one million to slightly over 180 million, Africa is a vibrant but also complex territory with different economic, social, cultural, political, security and risk profiles.

“Possibly the biggest misconception about Africa’s insurance industry is viewing Africa as a country, rather than a huge continent with 54 culturally diverse markets, with each market having its own requirements. Applying a global template approach to doing business won’t work in Africa,” Dr Oyetunji said.

He suggested that prospective foreign players consider partnering with local companies to gain insights into the markets and acquire the much-needed local knowledge. “Global insurers may find that the local skills may not necessarily be as expected, but the understanding of the local markets in terms of the people, their culture, their needs and their environment will be invaluable,” he explained.

Agreeing, Mr Granier said that for every market an insurer wants to enter, it is key to understand and adapt to local market specifics. “This is why we have chosen to focus on the insurance of businesses, starting from very small ones. We also think that microinsurance could become a great way to provide an easier access to basic coverage to people who today cannot afford minimal guarantees. This also means inventing new ways to access those customers, often through partnerships with mobile telephone operators, for instance.”

Exciting times ahead

Despite the challenges, including the risks of political instability, terrorism and pandemics, this is an exciting time to be active in Africa. With many of its economies now transiting from resource exporters to consumer markets where around 65% of its population is under 35, the region is one of the few bright spots on the back of a weaker global economic outlook.

To realise the opportunity, insurers should adapt their strategies according to local market characteristics to successfully expand in Africa.