Thanks to the maturity of its players, Morocco’s insurance market has preserved a leading position in the Arab World and Africa. However, life insurance needs to overcome the growth challenges, and sound regulatory initiatives will be required to expand the pie.

Morocco is said to be the only consolidated insurance market in the region, where just 17 providers write around MAD27 billion (US$3 billion) in premium income. It is the third-largest MENA insurance market after the UAE and Saudi Arabia, and the second-largest African market after South Africa. Ten providers belong to five groups, which further consolidates the marketplace. Six direct insurers control over 72% of the market – Wafa Assurance, RMA Watanya, Axa, Saham, Sanad and Atlanta.

“The market is not fragmented as even small players generate considerable income. This shelters the market against any kind of rate cutting or unprofessional competition and preserves the market balance,” noted Mr Mehdi Tazi, Chairman of Saham Assurance, Morocco’s largest general insurer in terms of GWP.

Self-regulated marketplace

The market discipline is clearly demonstrated in motor. A nightmare in most Arab countries, it is a stable and profitable line in Morocco despite the tariff being lifted in 2006. Motor accounts for over 31% of the market and is growing steadily.

“None of the operators are willing to cut the price as we all know this will have an adverse impact on the companies’ results. New entrants might resort to such techniques, but all the players are well-established, which lowers the incentive to enter a war price,” added Mr Tazi.

Medical, however, is under pressure to improve its results as its combined ratio has exceeded 100% over the past few years. “Players realise the importance of improving the technical results for medical, and the performance has improved in 2014. While competing, providers are communicating and discussing ways to preserve a healthy marketplace,” he said.

Slower growth for life

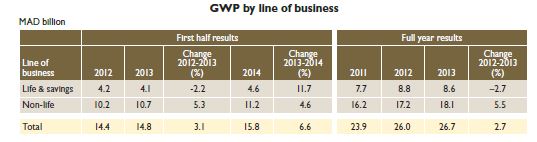

Historically, the size and distribution model of life insurance have been a salient feature of the Moroccan insurance industry. The life business, the second largest in the continent after South Africa, accounts for 32% – or MAD8.6 billion – of the overall market, and distribution is dominated by banks.

In 2013, however, the life business dropped by 2.7%, compared to the 14.5% growth rate achieved in 2012. This has been attributed to the overall slowdown in the country’s economic activities as Morocco continued to witness the impact of the Eurozone crisis in 2014, observed Mr Tazi. “For instance, economic growth in 2014 was expected to be around 4.7% but now, it is doubtful that it can reach 3%.”

Some market experts attribute the lack of growth in life to a heavier focus on investment than on protection. This has to do with the banking dominance, with an estimated 90% of policies being written by banks. “Our lack of a banking affiliate has been a major reason for Saham not to expand in life operations. To sell life insurance in Morocco, there must be a banking channel,” noted Mr Tazi.

This has consequently affected individuals as many have withdrawn their savings policies due to economic constraints, opined Mr Mohamed Zerrei, Associate at Grant Thornton Morocco. “Moreover, recently individuals are seeking alternative channels of investments because of declining returns from life policies. Real estate investments, for example, are gaining ground at the expense of financial tools such as life insurance,” he added. This could explain the 30% and 34% drops in annuities premiums in 2013 and 2012, respectively.

Mr Zerrei warned that the life business is expected to receive another blow with the government’s decision to abolish the tax exemption in 2015. “Besides seeking extra sources of income, the government justifies its move by saying that pension contracts benefit mainly those who have high revenues.”

Life group contracts in Morocco are subject to full tax exemption, but the government is proposing a 10% scheme.

Insurers are lobbying to reverse this decision and trying to bring the exemption to some middle ground. The tax exemption is supposed to make saving in life contracts more attractive, which should help the insurance sector remain as a major investor in the Moroccan economy. “But even if this happens, it will cast shadows over the life insurance market,” said Mr Zerrei.

Economic hurdles

The Contrat Programme, launched in early 2010, mandates a set of liability covers while requiring insurers to invest in certain activities to stimulate the national economy. However, the initiative remains inactive, and this could largely be due to the changing political environment, with major socio-political developments in the past three years leading to continuous changes in the government’s local policies. In addition, overall economic conditions in the Kingdom has put strains on the possibility of adopting new initiatives – particularly when the private sector is involved.

Against this backdrop and the fall in life operations, the Moroccan insurance sector registered a modest growth rate of 2.7% in 2013, compared to 9% in the previous year. This picked up in the first half of 2014 with the life segment witnessing growth of around 12%, while non-life operations increased by around 5% compared to the same period in the previous year. Overall growth in the first half reached 6.6%, against 3.1% in the same period in 2013.

Though promising, it is doubtful that the market will grow significantly, said Mr Tazi. “Again, it is due to the overall economic condition. The Moroccan insurance market is very promising and in good shape, but the economy is not booming and insurers are not growing as they used to.”

He said this is one of the major reasons for big players to seek growth opportunities in Africa. “Saham Group has been expanding in several African markets which have seen outstanding economic growth, reaching 15% in countries such as Angola and Nigeria.”

At least three of the largest local operators have branched out to African markets, mostly on the heels of their banking partners.

Making room for takaful

There has been plenty of interest surrounding takaful. A draft law was supposed to be launched last year, but reports now say it will be introduced in the first half of 2015, along with the sukuk law and other Islamic finance regulations.

The regulator is taking its time to ensure optimal outcomes, and players have agreed to start with family takaful to complement Islamic banking operations. This is expected to stimulate the life business and overcome any religious obstacles, if any. Several players, particularly the large ones, are interested in takaful and have the necessary tools to launch operations, and a legal framework should pave the way for this to take place.

Though some might doubt the significance of takaful contributions, it will be a means to attract foreign investments, particularly from the GCC region.

Regulatory reforms

This year may also see the emergence of the long-awaited independent insurance authority for Morocco, taking over the Insurance and Social Security Directorate at the Ministry of Economy and Finance. The Directorate has come a long way in adopting new regulations and updating the laws in the Kingdom. However, independence will give more authority to the regulator to enforce new measures and leave a more lasting impact on the market in general.

New solvency measures are also expected to be enforced in 2015, focussing on risk-based capital and specific processes designed for the Moroccan environment. The Directorate has been discussing these matters extensively with operators to ensure compliance and preparedness among market players before the measures are enforced.

“Basically, what the regulator wants is to link the solvency margin of the insurance company with its exposure to risks.

New procedures will be introduced, addressing risks such as underwriting risk, premium collection, and bad debt. We are positive about the new reforms as they will prevent companies from under-pricing, and help them stay prudent,” said Mr Tazi.

A financial hub in the making

Mostly unaffected from the Arab Spring, Morocco has remained as a safe haven in the region. The Kingdom has moved swiftly since 2011 by issuing a new constitution and addressing the country’s thorny issues. Though this has caused some delays in issuing new legislations, efforts have been made to promote Morocco as a regional financial hub and a reliable gateway to the rest of Africa through the Casablanca Finance City (CFC), replete with encouraging tax and investment conditions. “A special ‘fast lane’ was founded to ease the process in this direction,” said Mr Tazi.

Morocco is well-positioned to assume this role, he added. “The country offers a decent standard of living for Europeans who are interested in doing business in Africa, and local airlines fly to key African cities on a daily basis. In addition, the legal environment is conducive for foreign investors.” The outcome has so far been positive as international and regional players such as AIG, Partner Re and Trust Re have established a presence in CFC, either directly or through partnerships.

The project is a good opportunity for Morocco to attract foreign investments and further fortify its position as a financial powerhouse in Africa, said Mr Zerrei. “It is also part of the Kingdom’s recent policies showing more openness towards foreign investments, whether in reinsurance or other financial activities.”

Preparing for growth

By the end of 2014, following the severe floods in southern Morocco, the government revived the long-standing issue of mandatory Nat CAT insurance covering risks such as earthquakes and tsunamis. The programme was proposed around five years ago with the national reinsurer, SCR, put in charge of implementation, but it was overall under the regulator’s scrutiny to ensure effectiveness. The initiative is now likely to take shape this year.

Such moves will give broader scope for the industry to expand. The 3% insurance penetration level, though one of the highest in the region, indicates great potential.

As a leading regional market with professional players, issues such as underwriting discipline, price competition and capacity issues are not among the market’s main concerns. This makes Morocco a good example for other emerging markets. Yet, a lot more can be done to reach excellence. With the regulatory and operational measures expected to take place soon, the year ahead looks promising.