Sentiments are positive in Tunisia as it enters a new political era. Similarly, there is a sanguine outlook for the insurance sector with its new five-year strategic plan to increase penetration and take the market to a higher level.

Many developments have been taking place over the past four years since the 2011 revolution which sparked changes within Tunisia and the Arab world. A new constitution has been drafted, a new president has been elected and hopes are high for a better future.

The journey has not been easy, however, although there are signs of recovery despite the terrorist attacks in March. The country achieved a 2.8% economic growth in 2014 and this is expected to hit 3.7% this year, along with an improvement in the confidence in the North African economy as socio-political tensions ease, said the IMF.

A new strategic plan

In cooperation with the regulator, the Comité Général des Assurances (CGA), the industry is in the process of launching a five-year Contra Programme (2015-2019) to carry out structural reforms for the sector. The project aims to develop individuals and institutions, improve the level of services, and strengthen insurance companies’ financial capacities and solvency.

“We expect the Programme to increase the role of insurance in supporting the national economy and increase savings to contribute to economic prosperity,” said Mr Lassaad Zarrouk, Chairman of the Tunisian Federation of Insurance Companies (FTUSA).

He described the market growth in 2014 as satisfactory. Preliminary results show that GWP reached TND1.53 billion (US$782 million) last year, an 8% growth over the preceding year and in line with the average growth rate for the five-year period from 2009 to 2013.

“The sector continues to recover after 2011 and results are gradually improving,” Mr Zarrouk added.

Bridging the life and pensions gap

Life insurance has been the fastest-growing line, with initial results for 2014 showing growth of 17% to TND259 million, accounting for 17% of the market GWP.

The future of the Tunisian market is in life, with savings gaining in importance, said Mr Zarrouk. However, most business comes from policies related to banking loans. “Therefore, we cannot claim that life insurance enjoys a strong position in Tunisia. Pension funds are starting to suffer from huge deficits, and this is expected to aggravate in the medium term. The government has started to discuss pension reforms, and this shows the political will to change the system. It presents a golden opportunity for insurance companies to position themselves in this area.”

He added that Tunisian insurers should also launch products in areas such as savings, income protection and education to prepare for demand, while creating standalone life insurers with sufficient human and IT capacities could be a good strategy to improve the quality of the life business.

Tax exemptions have promoted life insurance sales among individuals, but on the corporate side, the Ministry of Social Affairs has yet to allow more facilities to tie life premium payments with the social security system, Mr Habib Ben Hassine, CEO of Maghrebia Vie, noted.

Mr Ben Hassine said insurers’ pension products can largely provide an alternative for individuals. In general, regulations should be flexible to encourage insurance – life in particular. “They should keep up with developments in distribution and IT to expand operations in Tunisia,” he said.

Improving life distribution through banks

Maghrebia Vie, the country’s largest life insurer, grew its GWP by 9% in 2014 to TND40 million. The company intended to achieve more but was hampered by distribution, particularly with the banks, said Mr Ben Hassine.

He pointed out that despite the several bancassurance agreements inked in the past, there has been limited success in increasing sales from this channel. “Unfortunately, banks still do not understand the benefits from using bancassurance to obtain a capital-free commission,” he said, adding that banks tend to avoid selling savings products for fear this will affect their own similar products. “However, when the bank and insurer belong to the same shareholder, this problem is overcome because income goes into the same pot.”

The future of life insurance lies in bancassurance, he opined. “Distribution is much more successful through banks. In France, 82% of the life business is done through bancassurance. It is not only because banks have the data, they can also set achieveable sales targets for their branches.”

This is probably most evident in the case of Wafa Assurance, a unit of Morocco’s Attijariwafa bank. Though it opened less than three years ago, its income has grown immensely, making it one of the leading life providers.

Bancatakaful bearing fruit

In the case of Tunisia’s first and largest takaful provider, Zitouna Takaful, its synergy with Zitouna Islamic Bank over the past two years have started to bear fruit, said CEO Makrem Ben Sassi. Bancassurance accounts for around TND4 million or 20% of the company’s portfolio, mostly from life and assistance policies. “Bancassurance in Tunisia started around 10 years ago and it has been a good experience, but still needs to be developed in order to obtain more benefits,” he said.

The regulator and association are analysing the best ways to develop this channel and hopefully there will be enhancements in terms of the range of products allowed to be sold through bancassurance, he added. Life, personal lines and agriculture covers may be offered, but general lines such as motor and fire are banned.

The market’s second takaful operator, El Amana Takaful, is also eyeing bancassurance opportunities. With Al Baraka Bank, its parent company, changing from an offshore to an onshore set up, both parties have signed a distribution agreement starting March 2015, noted Mr Abdellatif Chaabane, Managing Director.

“This will open wider opportunities for the company, especially in personal lines,” he said. “Everything relating to savings and pension is of great importance in Tunisia. We will pay extra attention to this area in the coming years, especially with the unsustainability of national social security funds.”

Challenges in distributing takaful

Setting up 32 sales points – including company branches and agencies – in its first year of operations in 2013 is a sign of strength for the company, noted Mr Chabaane. “Our efforts in the first year focussed on improving the network and strengthening relations with clients. We managed to spread across the country in the first year.”

However, under the takaful law which was passed in July 2014, existing agents are not allowed to promote takaful products. “They are restricted to selling conventional insurance only. This ruling is not based on the Shariah rulings, according to many scholars. The broker is just a distribution channel.”

This is among the challenges facing takaful, pointed out Mr Chabaane. “The law has deprived El Amana Takaful of using our shareholders’ networks, which was part of the plan when the company was being set up,” he said. The three insurance companies behind El Amana Takaful – Comar, Astree and Carte Assurance – each own 18% of capital.

Another key challenge is the protection protocol, which gives preferential treatment to certain companies following the incidents of 2011 to compensate for their losses. “Hopefully in 2015, this will be lifted and open up opportunities for us to access big accounts. It will also give clients a wider range of choices, and some may prefer Shariah-compliant insurance.”

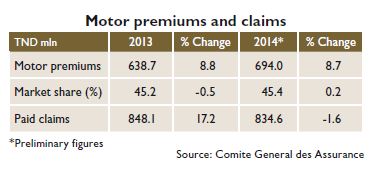

Dealing with motor losses

After the 2005 insurance law solved the motor issue following several years of losses, there were seven years of improvement in results before competition intensified, pushing players to cut prices of comprehensive covers, since compulsory TPL prices are fixed by tariff.

Post 2005, the cost of paid claims fell by almost 25%. “But immediately after the law on this was passed, insurers agreed to reduce up to 20% of comprehensive cover prices, believing this would not affect profitability. They were mistaken. The motor TPL tariff was increased by 10% starting March 2015 but for the sake of the public, the same percentage has been reduced from other lines such as fire. This is a first step to deal with the issue,” said Mr Ben Sassi.

Zitouna Takaful decided to learn from experience by writing a balanced motor insurance book, and continuously monitoring its performance, he said. “The structure of our motor portfolio is healthy. The TPL loss ratio in the market is around 300%, while in comprehensive, the loss ratio is around 40%. We are striking a balance with a loss ratio of less than 100%. The company’s TPL portfolio is around 20% of our motor business.”

According to Mr Zarrouk, losses and traffic violations have surged since January 2011. “Roads have become more dangerous than ever with death, injuries and material damages increasing to unprecedented levels. There is also the issue of fake accidents.” There is a need to improve risk management and enforce laws, he added.

Niche markets for takaful players

El Amana Takaful is making efforts to attract new social segments to increase market penetration, said Mr Chaabane.

The company plans to offer Umrah and Hajj products, while in microtakaful, it wants to reach out to those not covered by medical insurance, which number around three million, or a quarter of the population. “We are discussing the plan with the Farmers’ Association and other microfinance institutions to come up with the best means of tackling this area.”

Microfinance is also on the radar for Zitouna Takaful, said Mr Ben Sassi. “We are in talks with some institutions to offer products addressing the needs of small businesses. Besides looking at it from a provider point of view, we consider it part of the company’s social responsibility to give to the community and help those in need. It is in the spirit of takaful as well.”

New licensing on hold

The new law has put a stop to new licences, be they conventional or takaful. However, a study done by the regulatory authority expects takaful to account for 9-15% of the market by 2018-2019, and the number of operators at three to five. There are currently three takaful operators in Tunisia, a number that is “sufficient for the present phase”, said Mr Chaabane.

Mr Ben Hassine is in favour of separating the life and non-life branches for efficiency and to benefit from specialisation. However, life insurers should be allowed to sell both medical and life products, he added. “There should be cross-selling as clients always link the two products. This is to help the market expand life operations – a goal we are all hoping to achieve.”

Current regulations ban life insurers from writing medical. Mr Ben Hassine suggested a system whereby insurers can write lines of choice upon meeting certain capital standards for each line. “Licensing should be on an operational, not technical, basis. A company interested in writing certain business lines should pay the additional amount of capital. The regulator should be flexible in this area especially because it has to do with life insurance, which it needs as much encouragement as possible.”

This will help further expand the market, increase life penetration and encourage specialisation, he added.

Developing products and services

Medical is among the fastest-growing lines in Tunisia. “Maghrebia Group has invested heavily in IT to improve services. Clients appreciate the improvements and accept higher prices. Medical can be profitable if there is prudent underwriting and a good level of liquidity, especially for corporate accounts,” said Mr Ben Hassine, expressing hope to see amendments in the law to help grow life and medical in tandem.

Maghrebia Vie will continue to invest to develop the well-being of the market, either by introducing new products responding to clients’ needs or by training and developing its workforce. The market is promising and requires players’ efforts and greater flexibility from the regulator, he added.

Takaful makes headway

Benefitting from being the first takaful company in Tunisia in 2012, Zitouna Takaful generated TND9 million in gross contributions in 2013 and this jumped to TND20 million in 2014. Though this was from a low base, acquiring a 1% market share in the second year of operations was a big achievement for the company. “This is very positive, especially since the majority of business is new,” said Mr Ben Sassi.

Zitouna’s profitability is in line with its business plan, he added. “We incurred large expenses at the beginning and we are now amortising losses. If it were not for the circumstances of 2011, Zitouna could have distributed profits this year. Hopefully, next year will see the beginning of our surplus distribution.”

El Amana Takaful’s contributions in 2014 reached TND5.3 million before tax, while net income registered a loss of TND 1.3 million. “This is in line with our planned establishment expenses. Overall establishment expenses will be amortised over the coming three years. El Amana Takaful intends to distribute surplus to policyholders in 2016,” said Mr Chaabane.

For 2015, El Amana Takaful could obtain a market share of slightly less than 1%, “which is very impressive for a start.” In 2014, motor accounted around 67% of its portfolio, medical accounted for 13%, and life contributed 11%. “Motor has the lion’s share, reflecting the market. However, we are priced above the market, and most of our business is corporate.”

Local player seeks regional role

STAR Assurances is the market’s oldest player and largest income generator with TND259 million in GWP in 2013, a market share of 18%. It expects GWP to have increased by 11% last year and the plan is to distribute profits for 2014.

“This is mainly to convey the message to our shareholders, especially foreign shareholders, that STAR is doing well and the Tunisian market is promising on the investment level,” said Mr Zarrouk, who is also the CEO of STAR.

The period covered by STAR’s previous five-year strategic plan (2010-2014) was characterised by unstable market conditions, said Mr Zarrouk. “The next plan intends to modernise, support and strengthen the company on all levels so that by the end of 2019, STAR can expand locally and regionally. We have been working hard to improve our services and introduce new products, to position STAR as a regional player by 2019, tapping on our strategic partner Groupama to expand into African countries.”

A market in action

Despite the challenges, Tunisia’s insurance market continues to develop. The achievements in 2014 and the beginning of 2015 bode well for the years to come. Restructuring FTUSA to become a more agile body, moving to solve the motor issues, having the will to expand the life market, and forging a five-year plan are promising signs. Implementing these changes, however, will be the real test of success.

|

Political violence risk in Tunisia

Mr Chris Parker, Head of Terrorism and Political Violence at Beazley comments on whether the Bardo museum attack in March has led to any real impact on the political violence market.

“We haven’t seen an increase in the number of political violence enquiries for risks in Tunisia specifically following the attack in Tunis. However, the number of enquiries we have been receiving over the past six months has increased, and this could be attributed to the various ‘lone wolf’ attacks that have occurred in Paris, Sydney and Copenhagen over that time. These sorts of attacks have served to raise people’s awareness and remind them that terrorism and political violence attacks can happen anywhere and anytime.

“It is unlikely that there will be much impact on the market following the Bardo museum attack in Tunis since there is not a great deal of exposure in Tunisia. I am unaware of any claims in Lloyd’s as a direct result of the attack and therefore it is unlikely that there will be any movement in the premium rates charged for Tunisian exposures. It may cause some markets to review their existing book of business within the region but it is unlikely to have any impact on the market as a whole.”

|

|

FTUSA forges ahead in a new spirit

The Tunisian Federation of Insurance Companies (FTUSA) has undergone major restructuring to improve its efficiency and play a bigger role in reforming the sector, said Chairman Lassaad Zarrouk.

The year 2013 witnessed the start of greater momentum for the Tunisian insurance sector; 2014 was a continuation of this with more improvements in size and quality of business, said Mr Zarrouk. This year will see the beginning of several ambitious projects for the sector, starting with the reshaping of the Federation’s structure, he added.

Last March, FTUSA changed the structure of its board by reducing elected members from 23 to 12, representing all insurance companies. Their terms have also been extended from two to three years. Mr Zarrouk considers these changes as paving the way for the Federation to making strategic changes. The changes were made for the board to become more agile and efficient in making decisions, he said.

New direction

In general, FTUSA will be adopting a new direction, said Mr Zarrouk. “There is a strong will towards consolidation, mainly through mergers, which could lead to the creation of large insurance providers. Size has become essential in competing and succeeding.”

The move towards mergers is hampered by the lack of political will and some companies’ reluctance. However, there are signs that some companies are mulling over it.

FTUSA, meanwhile, has its own plan for the coming three years, based on the following:

• Developing the quality of services to increase the public’s interest in taking up insurance;

• Solving the problems of financially troubled insurers through enhancing financial and solvency standards, corporate governance and internal auditing;

• Modernising the sector’s IT standards in data exchange; and

• Encouraging mergers to prepare insurance companies to face internal and external competition and strengthen their positions.

|