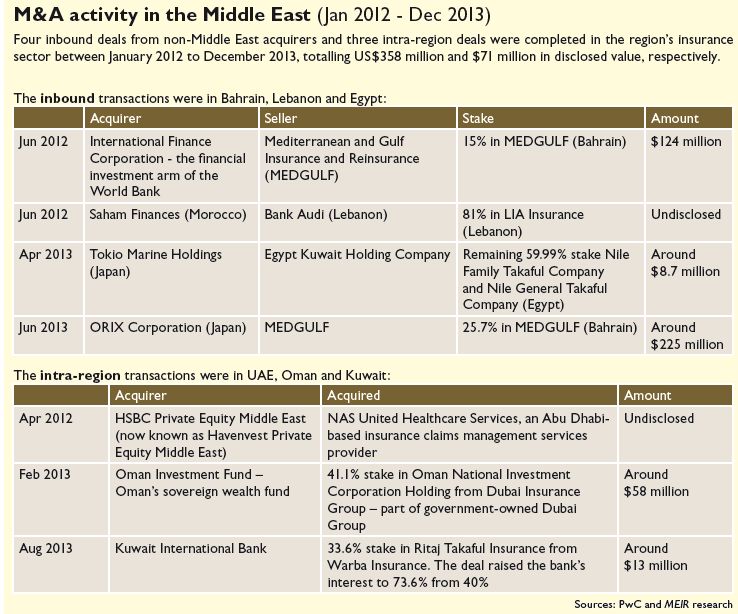

The market has been rife with M&A announcements and rumours of late – signs that such activities in the insurance sector may pick up soon.

There have been some encouraging signs that M&A activity is picking up steam in the insurance sphere, with several entities publicly stating their interests to acquire or sell in recent months.

In late May, AXA Group and its UAE partner Kanoo Group received approval to acquire a majority shareholding in the ADX-listed Green Crescent Insurance Co (CGIC). As part of the deal, AXA and Kanoo Group will be the primary investors of a capital increase in CGIC of AED100 million (US$27.2 million) via a convertible bond instrument. The move would push CGIC’s paid-in capital to AED200 million upon conversion.

On 27 July, Abu Dhabi-listed Islamic insurer National Takaful Company (Watania) said its majority shareholders had agreed to sell stakes to strategic investors from the Gulf region, while the National Bank of Ras Al Khaimah (RAKBank) disclosed on 24 July its intention to acquire a majority stake in RAK National Insurance.

Earlier that month, Oman International Development and Investment Co (Ominvest) approached fellow investment firm Oman National Investment Corp Holding (ONIC Holding) to explore a possible merger. ONIC Holding is active in life and general insurance through its subsidiaries and associates, including National Life & General Insurance, Al Ahlia Insurance, International General Insurance Holdings and Takaful Oman Insurance.

Meanwhile, there have been speculations that four insurance companies in Lebanon could sell their portfolios to larger companies. However, the Daily Star, which reported the news, did not disclose any names. There has also been speculation that RSA might sell its Middle East operations as these were not part of the UK insurer’s core markets, comprising UK & Ireland, Canada, Scandinavia and Latin America. RSA is looking to raise GBP300 million (US$506.3 million) this year through disposals.

Market conditions

The three proposed deals in July come at a time when both regulators and various stakeholders are renewing calls for consolidation in the insurance industry to create more players of critical mass and avoid cut-throat competition.

“Overcrowded and fragmented” are common terms used to describe the Middle East insurance market. While the insurance sector has generally seen positive growth in recent years, it still has low levels of penetration across the region. Almost all the markets are suffering from over-supply, a lack of skilled staff and expertise, and a need for product innovation. Many players lack scale to thrive, both geographically and within their domestic markets, a key factor driving consolidation.

Mr Rajeev Patel, Director at Deloitte Corporate Finance, said current market conditions are perfectly set for consolidation in the short to medium term. He added: “Regulators have long called for consolidation, however, we have seen little historical activity mainly due to the underlying underwriting performance, perception of captive insurance arrangements, unattractive valuations and complicated shareholdings.”

The inevitability of consolidation is further reinforced by the increasing sophistication of the larger insurers in terms of underwriting models, external credit ratings and their stronger bargaining power with reinsurers, and by increasing customer expectations in terms of services offered, according to PwC in a recent report.

Gap in price expectations

While recent trends are positive, gaps in price expectation are a common barrier that can stall potential deals. “There is a significant gap in pricing expectations between buyers and sellers – this has caused a number of potential deals to fail and may take more time to correct,” said Mr Sam Evans, KPMG’s Global Insurance Transactions & Restructuring Lead.

Recently, Bahrain National Insurance, a wholly-owned subsidiary of Bahrain National Holding (BNH), said it was not going ahead with its majority acquisition of Al Ahlia Insurance as “the selling shareholders of Al Ahlia Insurance were unable to reach with BNH an agreement on valuation that would satisfy both parties”. Both parties eventually agreed that it was not appropriate to proceed with transaction.

Earlier, in March, Oman’s Al Anwar Holding announced that the plan to merge its subsidiary Falcon Insurance with an unnamed insurer had failed. In a filing to the Muscat Securities Market, Al Anwar said discussions on the deal were called off as the other insurer felt that the terms for the merger were “not mutually agreeable”.

The bid/ ask gap needs to narrow, PwC said, noting that sellers need to be realistic on pricing expectations – holding out has proven costly for some players in terms of capital value erosion. Prospective acquirers may also need to revisit their bid valuations in the light of compelling market growth dynamics and the continued restrictions on new market entrants, while not ignoring the political risk factors in their calculations, it added.

On a positive note however, “the failure of a number of recent deals may lead to closer pricing expectations between buyers and sellers”, said Mr Evans.

Industry and demographic fundamentals in the Middle East are forecast to be strong over the next five years or so, with population growth, under-penetrated markets and demand for insurance among youths expected to continue driving the industry, said Mr Patel. “These factors alone could improve industry profitability and could help bridge the valuation gap between buyer and seller,” he added.

Due diligence

Should the pricing issue be overcome, there is also an additional hurdle of getting meaningful due diligence necessary for a successful transaction.

Transparency can be a key challenge during the deal process, said Mr Patel. “Given the highly competitive landscape of the industry within the region, understandably both the buy side and sell side players are reluctant to disclose financial and operational information, such as details of premium rates, significant policies and material contracts.”

Quality of information is also an issue, not only for M&A transactions but also for the industry as a whole. “It’s not unusual to see unreported KPIs, such as policy renewal rates, loss ratios and combined ratios at a sub-product portfolio level,” said Mr Patel.

Cultural issues

The region’s cultural environment can also complicate deals. Most insurance businesses in the Middle East are either government or family owned and are often culturally less receptive to M&A, or the businesses may not be mature enough to go through such a process.

Mr A R Srinivasan, CEO of Falcon Insurance, said: “The challenge with mergers in the GCC is that capital has never been an issue, and thus there has not been much impetus to companies to look for mergers. Furthermore, cultural issues and the need to have ‘control’ of the companies also act as a deterrent to look at mergers.”

Regulatory changes

A number of regulators in the region are taking steps towards promoting M&A activity by imposing stringent requirements.

In May 2014, nearly 10 years after deliberations first began, the UAE’s Federal National Council passed a draft companies bill that should go some way towards clarifying and simplifying the transactional process. Late last year, the Insurance Authority raised capital requirements for brokers and by August 2015, new regulations are expected to take effect to require composite insurers to segregate their life and non-life businesses. The move could trigger a surge in IPO activity and more importantly a split of “good” and “bad” insurance operations, which could help increase M&A activity too, said Mr Patel.

In Saudi Arabia, stringent regulatory requirements such as strict admitted assets, solvency rules and limitations on granting new licences are also also deemed favourable for M&A.

In Oman, the Capital Market Authority has increased the minimum paid-in capital for insurance companies to OMR10 million (US$26 million) from OMR5 million, which could see some insurers exiting the market and increase consolidative pressures in the sector.

Regulators play a key role in ensuring the solvency of the insurance industry and could enforce consolidation if the market is deemed too slow to act, said Mr Patel. “We have seen this in the more developed banking sector, where specific markets have undergone necessary consolidation to counter weak balance sheets as a result of external shocks to the economy. We are starting to see a similar theme in the insurance industry, where a number of rights issues have been authorised by the Saudi Capital Market Authority to help strengthen balance sheets, for example, and other markets could follow soon,” he added.

Solvency modernisation initiatives in the region, such as move towards IAIS’ Insurance Core Principles, are also expected to have a significant impact in terms of increasing capital requirements through the introduction of risk-based capital, and increasing the burden of regulation through the Own Risk and Solvency Assessment (ORSA) and other governance measures. The combination of these factors is expected to drive consolidation, said Mr Evans.

On the other hand, regulatory factors can also impact deal process, “with sometimes vague and changing regulations often delaying or prolonging deal processes”, noted Mr Patel.

Positive developments

Consolidation might take place as some new capital rules might be very constraining for small companies, said Mr Alexis de Beauregard, Chief Officer - Marketing and Retail Product Offering at AXA Gulf. “We could also see it happening for efficiency gains and economies of scale. This will also go a long way in providing opportunities for other players, both regional and international, to enter the market through acquisitions, but only if they make sense and offer good value for money deals.”

There is currently nothing to suggest that acquisitions will not pick up over the next 12 to 24 months, Mr Patel said. “Deal activity over the last six to 12 months in the GCC has picked up compared to this time last year, and we are seeing real interest in insurance businesses from family offices, private equity houses and foreign investors looking to set up shop in the Middle East,” he added.

“There are both positive and negative forces impacting on the region and therefore it is difficult to predict which way the market will go in the short term,” said Mr Evans. “In other regions, we are seeing a pick-up in M&A activity and this in itself may create a positive knock-on impact in the Middle East.”

Mr Srinivasan said deals in Oman, such as Dhofar Insurance’s portfolio acquisition and the merger of Al Ahlia Insurance with RSA Oman in 2010, have helped create significant growth and potential for the merged entities. “With the collaborative efforts, shared vision of both parties seeing larger and stronger insurance companies, and the support and the desire of the Capital Market Authority, I am hopeful of seeing more such mergers in Oman at least, and perhaps in the GCC region,” he added.

There are interesting times ahead for M&A with growing market and regulatory forces. Will the region finally reach its desired level of consolidation? Watch this space.